Industry Thought Leadership

5G as a Driver for Collaboration

March, 2020

Despite their revealing alternative name, ‘LTE (Long-Term Evolution) networks’, 4G networks created a major shift in both perceptions and adoption of communication services. This, in turn, led to the relatively early launch of the next evolutionary step: 5G networks.

Massive changes in data bandwidth provoked a tectonic shift in customer perceptions of what ‘mobile’ meant. I witnessed the revolution that was the 3G rollout, when, in rural areas, high (for the time) bandwidth together with competitive bundled pricing put mobile providers in direct competition with outdated fixed-line providers, effectively killing old-fashioned access networks. 4G development and wider smartphone adoption made this trend even more evident. 5G is now starting out in pretty much the same manner, with FWA driving its adoption.

At the same time, making the business case for network rollout is becoming ever more challenging, as new network generations emerge more rapidly and start to overlap with increasingly widespread OTT services and mature market penetration. It will take more than just ‘another, faster Internet’ to achieve acceptable ROI for 5G rollouts, instead requiring active analysis of both sides of the equation: optimising costs as well as increasing the value of services (or telcos’ position in value chains).

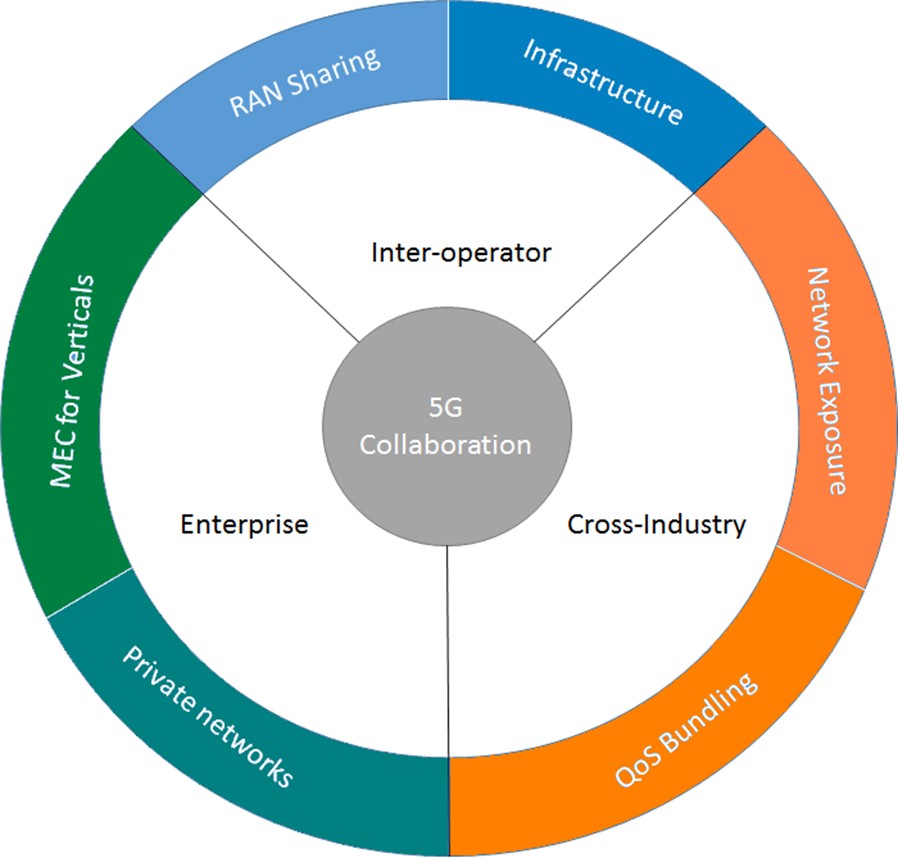

Different ways of managing costs are already being widely discussed across the industry. The 5G technology stack comes well equipped in this respect, thanks to both internal optimisation (based on virtualisation and cloud technologies) and the potential for collaboration. Together with pressing spectrum issues, RAN and infrastructure sharing are becoming key topics in these discussions, opening the door to cross-operator collaboration on a particular area or tower, or even on radio equipment. This has already started to create additional requirements for inter-operator settlement, but wider adoption, together with dynamic spectrum capabilities, will take place once network slicing technology has truly come into play, leading to more dynamic schemes to manage those settlement streams.

Another aspect to consider here is the growing interest in private networks. On the one hand, this approach will create local out-of-industry competition from large enterprises or vendors; on the other hand, a new niche will be created for CSPs, helping them to make their operations unit a profit centre as they collaborate with enterprises on spectrum and equipment leasing while launching managed services for these networks.

This approach is aligned with the next area for open collaboration with other industries: mobile edge computing, or MEC. Industrial use of 5G requires not only fast connectivity and high-capacity connected devices, but also extremely low latency and the capacity for fast and secure turnaround to local and specific apps. Currently, the focus on MEC applications is still relatively operator-driven, but having the capacity available for third-party applications and industry verticals will create interesting capabilities both for servicing enterprises and for collaborating (and competing) with cloud providers.

Another area of focus should be growing consumer revenue streams as new use cases become available to end consumers. Clearly, FWA and eMBB will drive 5G adoption, but they are unlikely to function as new revenue generation tools. Just as in the case of 3G and 4G, competition and consumer willingness to pay for access will drive rates down to previously established levels. Consumers’ focus is on end-to-end services, whereas data access is merely an enabling technology. It may get blamed for poor quality but will never be the centre of consumers’ attention (unless it is interrupted). And the price tag for connectivity is already fixed and well-defined.

There are two obvious ways out of this trap. One has already been tested many times and has proved less than successful. Many attempts to develop and promote ‘walled gardens’ have failed under the pressure of Internet services, both in pure communications and in entertainment services.

The other way looks more promising, and enjoyed proven success at earlier stages. Telcos are already monetising their access to end users by building alliances with key entertainment service providers as a retail channel. Direct carrier billing together with dedicated service-data bundles are becoming a relatively common feature. 5G architecture, along with the growing sensitivity of services to underlying infrastructure, will help CSPs to enrich this collaboration stream and acquire an additional role in value generation by opening up network quality management capabilities to their partners as a sellable asset. Building on the adoption of SCEF in the 4G era, 5G NEF – and proper monetisation of its capabilities – may become an additional factor that will help to keep these partnerships together. And as the ecosystem approach is spreading fast, making CSP assets available for ecosystem integration instead of just data transport or distribution may help CSPs to secure a more favourable position in the value chain.

To round things off, I would say that 5G architecture and the underlying technology open the door to many interesting collaboration streams with players inside and outside the industry. It is still early days for most of these use cases (and joint activities in cross-industry forums are helping to shape and test them), but the overall direction is clear and looks promising. From the BSS vendor perspective, these use cases generate new requirements and interesting challenges around monetisability and revenue generation. Nexign Digital BSS already incorporates capabilities to support most of these cases, but we are actively participating in industry forums and activities to make sure our customers get the most out of the opportunities opened up by 5G networks.